Our system for corporate moral rating in five dimensions

Please see Notice with important explanations and caveats about our ratings before making a judgment on a rating or verdicts on a company.

Our Rating Methodology is the practical way we have decided to implement the five pillars of our Rating Philosophy.

The first axis of our rating system covers the three dimensions, Degree, Speed, and Attitude. They measure what the company actually did – what, when, and how they did it. The second axis covers potential impacts, on the company itself through its Exposure (which equates to the Sacrifice it would be making), and on Russia through the Power the company had to wield (which equates to the economic impact it would have). We consider these two dimensions to be Moral Multipliers. They are different from the first three dimensions in that they quantify pre-existing factors that magnify the morality or lack of morality in corporate actions.

Exposure shows a company’s moral behavior in overcoming differing degrees of pain to do the right thing. Power is also part of a company’s moral behavior because it has a greater moral responsibility to act if it has a greater potential impact.

We investigate the first exit action of a company, what we call the Announcement and define it precisely to show what it covers. We measure how moral the company was, how satisfactory the Announcement is, using the first three dimensions of our rating system.

– The ‘What’ is about the Degree of action.

– The ‘When’ is the Speed of action.

– The ‘How’ is the Attitude of action.

A company should exit Russian commercial involvements completely if it is going to avoid supporting the Russian government and its economy. Many company Announcements do not involve a Full & Complete action. In our view, out means out – no ‘ifs’, ‘buts’, ‘mights’, or even ‘wills’. If a company wants a good rating from us, its withdrawal from Activities has to be total and unequivocal.

Therefore, the ‘Degree’ of withdrawal is crucial and companies making Partial or Incomplete actions are less moral than those making total actions, even though such companies are, of course, more moral than those who take no action at all. Many companies are announcing exits that are unsatisfactory in one or both of these ways and getting credit in the media for having exited.

For Degree, our goal is first to determine what Activities a company was involved with at the time of the invasion of Ukraine, then which of these it has or hasn’t stopped, and then how completely each has really been brought to a close. Analysis of Degree is the way we attack the tendency of companies to hide in Shades of Red .

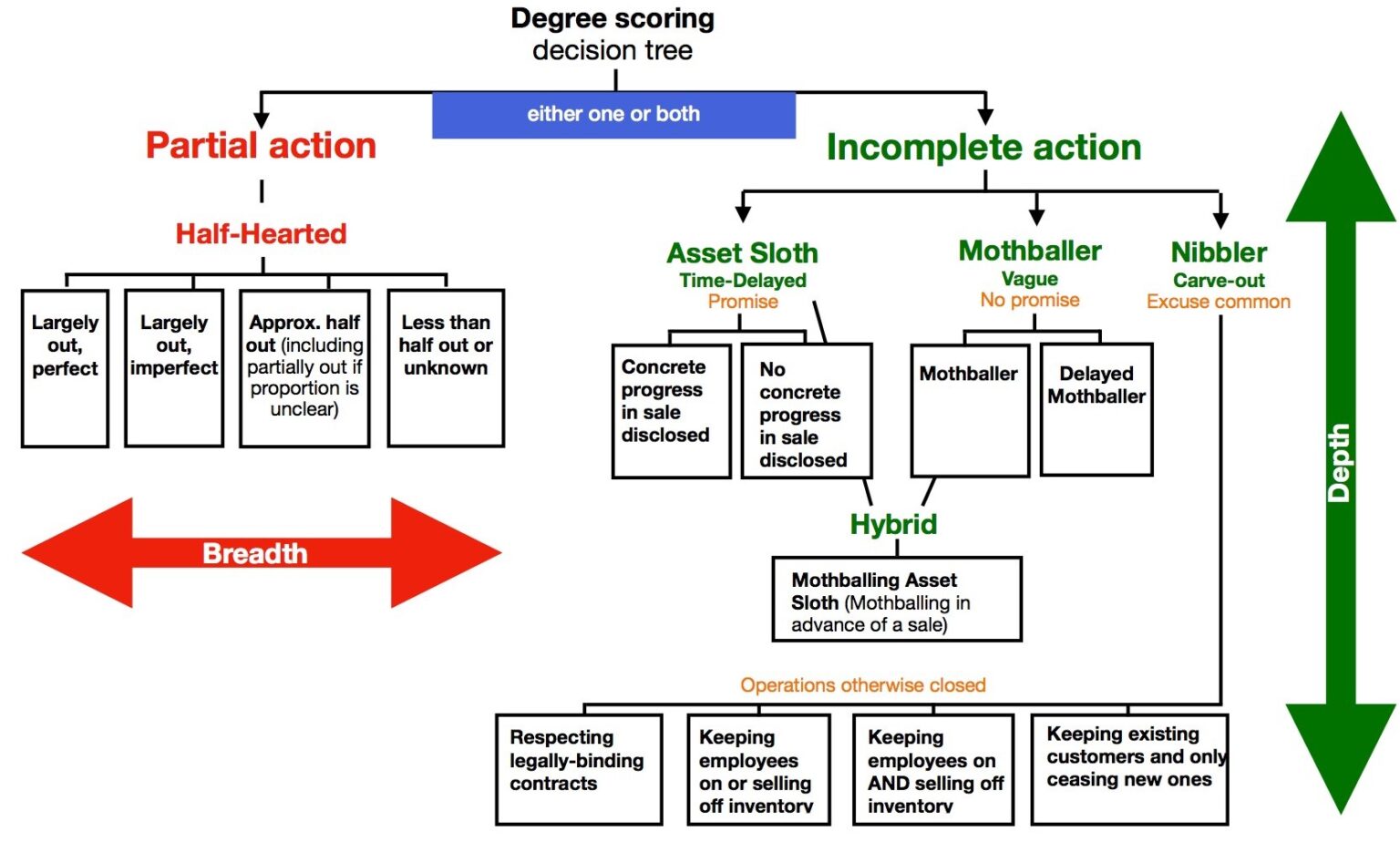

Degree thus looks at the extent of a company’s actions in two main senses, the Breadth of the action (number of Activities withdrawn) and the Depth (completeness of each withdrawal). There are two types of failure in an action.

The company may cut one discreet Activity and not another, for example by stopping exports but not imports, or stopping both exports and imports but not production in Russia. Or, it may close one factory but not another. We describe such an Announcement as a Partial. We call such companies ‘Half-Hearted’ , but that doesn’t mean the Activity being exited represents half of their total Activities in or with Russia.

When the withdrawal of one or more Activity is done in an incomplete sense, we call this an Incomplete. Incompleteness itself falls into three main sub-groups:

a) The Announcement says the company will sell its assets but doesn’t confirm it has actually done so. The Announcement often contains words like “is ceasing”. Indeed, they may never actually sell the asset and instead wait for world events to change only to announce that it is no longer necessary to do so. We call this a Time-Delayed Incomplete and the company an Asset Sloth.

b) The Announcement refers to suspending operations without saying the company will actually cut them properly (sell the asset). Such a company is basically mothballing its activities in Russia. The lights have been switched off but can be switched on as soon as the time is right. We call this a Vague Incomplete and the company a Mothballer.

c) The Announcement carves out something that causes the withdrawal to be Incomplete. These carve-outs usually occur with an excuse for the Incomplete aspect since disclosing incompleteness is controversial without a reason. We call this a Carve-Out Incomplete and the company a Nibbler.

The Nibblers close the operations but make carve-out such as keeping employees on the payroll, keeping existing customers, or continuing to sell inventory.

Companies cannot get a full score for Degree if their Announcements have any of these Partial or Incomplete deficiencies. And the more deficiencies companies have in Partial or Complete, the lower their Degree score will be: for example, a company making a Partial which is itself an Incomplete. Companies that later move from Partial to Full and/or Incomplete to Complete are eligible for Upgrade but only when they reach Full & Complete. However, the Announcement’s deficiencies or inactions are always reflected in our Indelible Ledger.

Since we believe companies have a moral responsibility to be transparent about what Activities they have and which they are withdrawing from, we look at the clarity of the Announcement and may mark down such imprecision or evasion. An imperfect announcement can result from one or both of: a) imprecision in facts (such as a company saying what it is withdrawing from Russia without disclosing what has with Russia and/or what it isn’t withdrawing); and b) imprecision of intention (such as a company saying it is suspending production due to supply chain issues which would leave open the possibility it may resume production at any moment since it has made no commitment to tying its decisions to Russia’s behavior).

If Degree covers one of several Activities (i.e. a Partial), our score takes into consideration that withdrawal compared to our estimate of how many Activities the company didn’t act upon, and also, where possible, their relative economic size.

We allocate a Breadth sub-score of up to 10 across the Full-to-very Partial spectrum from good to bad:

– Full, perfect

– Full, imperfect

– Largely out, perfect

– Largely out, imperfect

– Approximately half out (including partially out if the proportion is unclear)

– Less than half out or unknown

If a company has more than one exit event and we can see that our policy of scoring on the first action is going to lead to a lower Moral Rating versus judging the company on its cumulative Degree for the second exit date, albeit using the second date for Raw Speed Date, we use the more favorable alternative. This is because otherwise it would be better for a company to skip making its first action and announce both actions at the same time in order to get a better rating.

In case of an Asset Sloth, which makes a Time-Delayed Incomplete, it is clearly impossible to get inside the mind of a company that says it will sell an asset, to know if it will actually do so, or if it was just said to get the media off its back while it waits for world events to get it out of honoring its promise.

Therefore, we have an objective way of scoring this. After taking into account any concrete plans the company showed about a sale process, any Degree Score awarded will still reflect the fact that, regardless of intention, there is zero impact on the Russian economy so long as the statement remains a promise. If the Asset Sloth makes good within a timeframe, we can Upgrade it.

A sale of an asset to another foreign entity does not count as Complete according to our rules because it only results in one investor being replaced with another and therefore may not damage Russia at all. Companies are required to divest to the local market so that Russia is cut off from foreign investment and know-how as a result. Moving the asset, through a sale, to a different foreign owner is called a Circular Exit.

In the case of a Mothballer, which makes a Vague Incomplete, the company gets a middle-level Degree Score since it has at least stopped economic activity for now, with similar Upgrade potential if it sells the asset.

In the case of a Nibbler, which makes a Carve-Out Incomplete, depending on which of the sub-types it is, it gets a different Degree Score. Likewise, it has a chance for an Upgrade if it sells the asset.

A threat from Russia (for example to nationalize a factory) is no excuse for inaction and a company not acting because of such a threat will be scored as having failed to act. The company does, however, get credit for having been subjected to such threats through a higher Exposure score. Thereby, if it does the right thing and withdraws, the higher Exposure score will lift its resulting Moral Rating.

Our ‘out means out’ policy extends to companies claiming they cannot withdraw from legally-binding contracts. If this is their only deficiency, we give them a high score, but not complete credit, because we consider they have a moral duty to cut all ties even if they suffer economic consequences of not fulfilling their obligations. As we say, no one is morally obliged nor morally right to ‘do business with the devil’, nor doing business that supports the devil’s position.

We allocate a Depth sub-score of up to 10 across the Complete-to-very Incomplete spectrum starting with the best:

– Complete in Depth

– Mothballing Asset Sloth (hybrid) doing Mothballing in advance of a planned sale

– Incomplete Exporter/Importer, such as keeping after-sale servicing going in Russia to support exports, continuing to sell off inventory already shipped to Russia, or refusing to use Moral Force Majeure to break legally-binding agreements.

– Mothballer (Vague Incomplete): If a Mothballer keeps legally-binding contracts going, we will score as a Mothballer.

– Nibbler keeping either employees on or continuing to sell from inventory produced in Russia but otherwise closing all operations (a type of Carve-Out Incomplete)

– Nibbler keeping both employees on AND continuing to sell from inventory produced in Russia (a type of Carve-Out Incomplete)

– Asset Sloth disclosing concrete progress in, but not completion of, a sale (a type of Time-Delayed Incomplete)*

– Asset Sloth disclosing no concrete progress in sale (the second type of Time-Delayed Incomplete Exit)*

– Nibbler keeping existing customers or suppliers and only ceasing old ones (a type of Carve-Out Incomplete Exit)

– Delayed Mothballer (Vague Incomplete Exit) with plans to Mothball operations in Russia.

* If an Asset Sloth is barred from selling its shares in a listed Russian company, depending on other considerations, they should not receive any reduction in their Degree score since they may be doing the maximum, even though we cannot measure their intent. They can receive a full score for Depth.

* Note we don’t give such companies a score of 10 for Depth because they should use what we call ‘Moral Force Majeure’ to cut contracts, even if there might be a financial consequence in breaking them.

** If an Asset Sloth is barred from selling its shares in a listed Russian company, depending on other considerations, they should not receive any reduction in their Degree score since they may be doing the maximum, even though we cannot measure their intent.

Note: If an Asset Sloth engages in a Circular Exit, they cannot be Upgraded and their score is frozen at their original Asset Sloth level.

Note: If we give credit for an action based on media and the company has not confirmed it, the Depth Score will be 2 regardless of which type of Incompleteness it falls into.

In cases where the deficiencies are on both measures of Breadth and Depth, each sub-score out of ten is then multiplied so one is a fraction of the other, generating a score out of 10.

Speed is critical, not only because every day of delay is an advantage to the Russian government and economy, but also because speed is a dynamic thing.

We see cases of peer companies engaging in what we call Domino Exits (one company’s Announcement is followed within a few hours by one or more competitors that, regardless of moral considerations, can’t face the embarrassment of being seen to be behind others).

The corollary of this is that delay actually encourages companies and even non-peer companies also to delay. By contrast, once a point is reached where most companies have withdrawn totally in a sector, the pariah will not just be Russia but also the minority of companies that is still refusing to cut links.

Therefore, Speed of action is a critical moral measure in more than just the number of days following the invasion, but also in the sequencing. So, we take this into account by awarding Leader of Pack Bonuses and Chicken Penalties.

We allocate a Speed Score of up to 10 by taking into account five sub-elements.

Attitude covers the words a company uses about Russia to provide moral leadership as well as altruistic actions taken to support Ukraine.

The strength of a company’s words is critical because it can have an impact on Russia as well as a dynamic impact on other companies. Indeed, many major companies have spoken out against this autocratic regime where they have business interests. For this to become widespread, it needs momentum. There is an opportunity for a virtuous circle climate of taking action against Russia: companies not taking action can be pushed to do so not only by the actions of others but their words as well.

Companies start with those admonishing Russia at one extreme, which we call Denouncers . Then, there are the ‘Mealy-Mouthers’, who behave as though the war is no one’s fault but is very sad; then the Cowards, who give alternative or additional reasons rather than focusing on the war; and finally Strong Silent Types, who take actions in silence.

Speaking out against Russia is not only important for its impact but, like the action itself, speaking requires corporate courage because doing so might cause retaliation by the Russian government against companies in the future, or potentially criminal retaliation against managers.

Meanwhile, altruistic assistance is not only morally good in itself, but it also further pressures the Russian government by showing support for the injured party.

These two factors, which comprise our Attitude Score, involving moral efforts, are required components to receive a full Attitude Score. We calculate each sub-score and average them.

We allocate a Leadership sub-score of up to 10 to minus 5 across the ‘Denouncer-to-refusing to take sides’ spectrum from good to bad:

We allocate an Altruism sub-score of up to 10 depending on the valuation of the assistance to Ukraine as a percentage of its own profits, across the spectrum from 1.8% to less than 0.05% of after-tax profits. We may also value assistance in non-monetary forms, such as products or services.

Moral Multipliers reflect the pre-existing conditions of a company’s Russian involvement before it takes any action, and are measured at the time of the invasion. They act to multiply or leverage positively or negatively the moral behavior of companies in their Degree, Speed, and Attitude of action as scored above, or in their failure. The two Moral Multipliers are Exposure and Power.

This Moral Multiplier ‘second axis’ is about the increased or decreased morality of an action or its absence, which derive from these circumstances. Exposure changes the level of sacrifice involved (moral courage) and Power changes the level of impact involved (moral responsibility).

A company with less Russian Exposure has less shareholder interest to consider than a company with high Exposure. While withdrawing from Russia is the overriding moral responsibility of every company has to the world, and specifically the Free World, the willingness of companies to override shareholder responsibility in cases of high Exposure shows moral courage which we term Sacrifice.

Our Moral Rating takes into account how Exposure heightens or lessens the morality of withdrawal status. As an example, a company with a lot of Exposure withdrawing fast and properly gets a higher rating than a company doing the same actions if it doesn’t have to suffer so much pain. Meanwhile, a company refusing to withdraw from Russia that would have involved less pain gets an even lower rating than a company refusing to exit with huge Exposure because the latter company had less of a moral conflict to overcome.

Thus, high Exposure makes the good action better and low Exposure makes the bad action worse.

We look at the Exposure at the time of the invasion, in terms of the effect on the company financially for cutting all involvement with Russia. It is not measured on the basis of the company’s Degree of withdrawal but based on its entire Exposure picture.

We make our own estimate of Exposure after considering what we can discover about four principal ways to measure potential pain, considering both the near and longer-term prospects for financial suffering:

If the company’s Announcement discloses the total impact on profitability from all of its Activities, we will use the company figure, but it is rarely available. Otherwise, we start by analyzing exports and activities inside Russia separately, as follows:

We estimate Export Pain with a sub-score of up to 20 across a spectrum from 8% of revenues down to less than 0.4%.

If the company is exporting commodities, we reduce the sub-score in half, on the theory these will more easily find other markets. If we have information that the Russian exports are more or less profitable than the other revenues of the company, we will also make an adjustment.

We try to estimate the importance of any Activities inside Russia as part of the company’s overall economic picture. If we have info on Russian assets or equity, we calculate this as a percentage of the total. Likewise, if we have revenues or after-tax profits from inside-Russia operations, we calculate this as a percentage of the total. Otherwise, we try to use the number of employees in Russia as a percentage of total employees as a proxy for Investment Pain.

We apply one of these measures to Investment Pain with a sub-score of up to 20 across a spectrum from 8% of after-tax profits down to less than 0.4%.

We consider any Import Pain from any critical imports, which is rare. If it exists, after weighing up the above measure, we boost the result using our judgment.

Any threat made specifically to the company, or to the company’s sector, by the Russian government about withdrawing, whether the threat is made before or after the company’s Announcement, is credited on the basis that the company might have feared this risk as part of its decision. If this occurred, we boost the score using our judgment.

The final Exposure Score is capped the score at 10 and labelled as follows:

9 – 10 = Extreme

7 – 8 = High

4 – 6 = Average

2 – 3 = Low

1 = De minimus

A company that wields greater economic Power over Russia has a greater responsibility to take action. Or, put another way, if such a company doesn’t withdraw, it is supporting Russia more than a company with less Power.

Therefore, our Power Score is part of the Moral Rating based on the level of Power the particular company had. For example, a company with a lot of Power which remains involved with Russia gets an even lower rating than a company behaving the same way without such a high level of Power and associated moral responsibility. It is possible that a company with vast Power that remains partly involved in Russia could get a lower rating than a company with much less Power that doesn’t withdraw at all.

In short, high Power makes inaction even less moral.

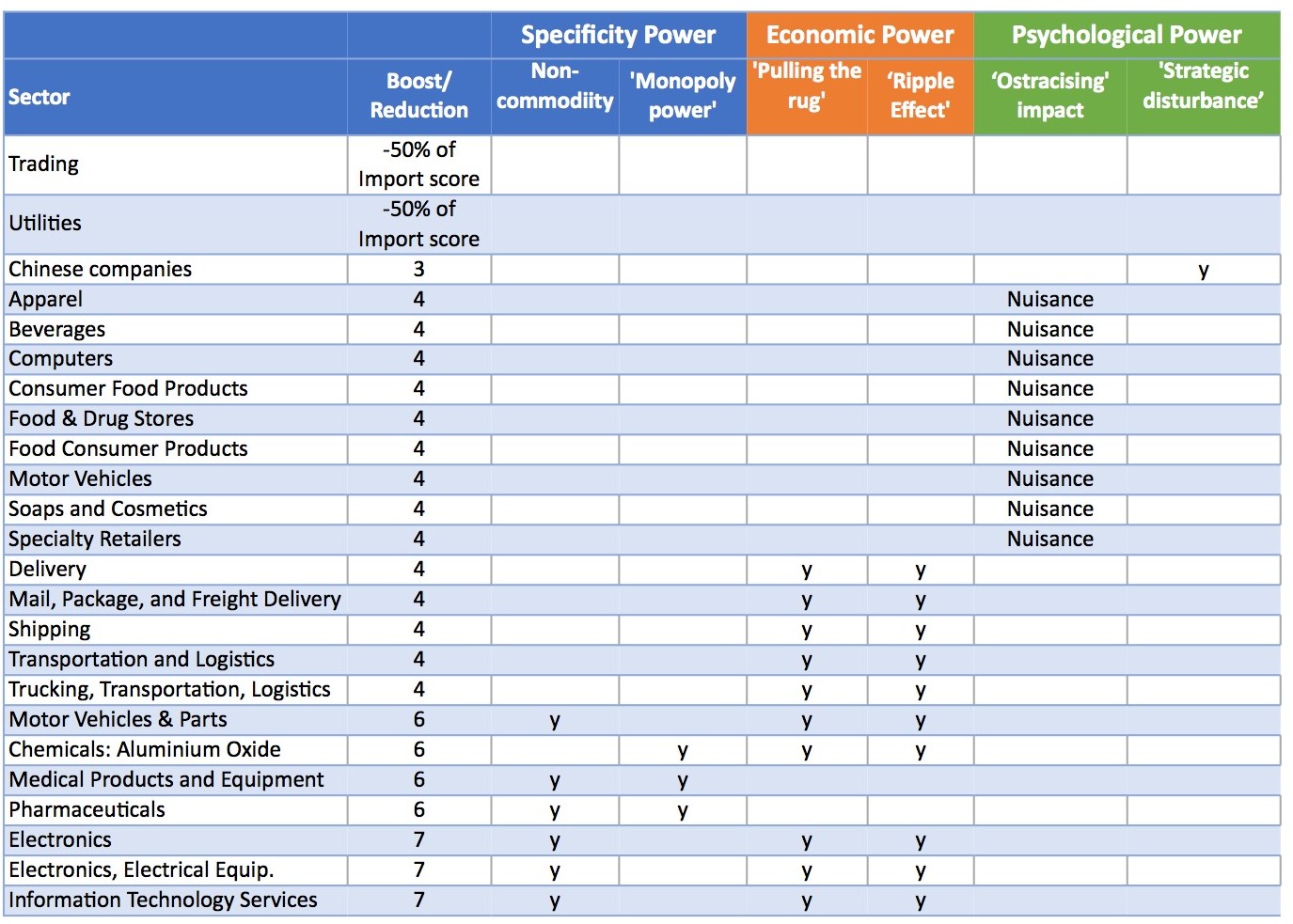

We estimate Power in terms of how much the company could impact Russia as of the time of the invasion. We look at the impact on the Russian economy and also the psychological impact.

We make our own estimate of Power after considering what we can discover about three principal ways to measure potential economic and other impacts on Russia:

We estimate Import Power with a sub-score of up to 20 across a spectrum from $1 billion or imports to less than $50 million.

We use the company’s Russian employees dependent on the company as a proxy to estimate Investment Power with a sub-score of up to 20 across a spectrum from 10,000 or more employees down to less than 500.

Companies often wield more Power than they think over Russia, by which we mean that their direct economic influence as employer/taxpayer/producer and as importer may be eclipsed, or at least augmented, by their indirect economic and societal Power as an exporter.

We look at this in terms of potential economic and psychological impacts.

We take into account if the company exports to Russia any product, component or service that could have an indirect or multiplier effect on the Russian economy, including its ability to attack Ukraine, particularly technology or components, the withdrawal of which could disturb the economy or market. Here, we monitor these economic impacts:

We also consider exports of goods or services, the withdrawal of which would have a psychological Multiplier Effect on consumers or damage the government’s strategies. Here, we monitor these categories:

We use this Multiple Effect menu to derive a boost or reduction to the Power sub-scores derived above:

Note that commodity sectors don’t get any boost because it is relatively easy for Russia to procure from companies and countries not participating in the boycott. This will persist unless there is a near-total embargo. To reflect the lack of impact of such sectors, where such a company imports from Russia, we apply a 50% reduction to its import sub-score.

After averaging the Import Power and Investment Power, we add the boost from any Multiplier Effect, which we cap at 10 and add a label as below:

9 – 10 = Extreme

7 – 8 = High

4 – 6 = Average

2 – 3 = Low

1 = De minimus

The scores for Degree, Speed, Attitude, Exposure and Power are all brought together to generate a company’s rating.

For simplicity, the ratings can viewed in three broad bands:

The real value of the rating system, however, is not these three broad categories but the finer definitions of the Moral Ratings and Moral Badges.

Each company receives a Moral Rating. Having generated five dimension scores for a company, these are brought together into a Moral Rating which ranges from 105 down to minus 14.5, This is computed using our Moral Algorithm.

This allows companies to be compared quantitatively down to more than a hundred moral levels.

For each company, the computation of the algorithm is shown in a pop-up over its Moral Rating. This allows readers to see the calculation from each of the five dimension scores through to the figure presented as the company’s Moral Rating.

Each company also receives a Moral Badge. The badges are permutation-driven labels or categories that combine different ranges of results for each of the five dimensions. An example of a badge generated by the five dimensions is ‘Speedy Near-Boycotter Martyr with great Attitude & Power’. The permutations generate approximately 60 different badges.

This means we have a word-based moral ladder, a bit like the moral hierarchy of altruism invented by the Jewish philosopher Maimonides nearly a thousand years ago.

Please read this section before making judgments about companies:

A statement by, or report on, a company about it stopping Activities, involving a meaningful action, which we monitored before the “Rating as of” date indicated for the company on our site. In the case of more than one statement being monitored, ‘Announcement’ refers to the first one. When we use related capitalized words like “Announced”, “Announced an exit”, or “Announcer”, we are referring to this same definition.

We purposefully do not rate statements or reports after the first one because the site’s purpose is to be an Indelible Ledger of the company’s initial action. Confining the information on which our rating and views are based to the first action is also needed, in order to measure the Speed and Attitude of the action. In some cases, if we think it would be fairer, we rate a company based on a statement or report that is later than the first one.

There is an Upgrade possibility but only when later statements clearly show the company has reached Full & Complete. However, this is presented separately and does not vary the underlying information presented for the five dimensions of Degree, Speed, Attitude, Exposure, and Power, and the associated Moral Rating, Moral Badge, and Verdict, which derive from these.

A company’s involvement with Russia we have monitored which may cover any type of business relationship, including these examples:

Financial and insurance relationships are generally impossible to monitor.

We seek to measure as many as possible of these business relationships in or with Russia, by default for the parent itself and, when we can, for the group, as of the time of the 24 February 2022 invasion of Ukraine.

When we refer to a company, or score, rate and comment on it, subject to the information we have been able to monitor, we may be referring to the Activities, Announcement or behavior of any part of its group including entities it has some control over.

Whilst we consider it is reasonable to expect a parent to make an Announcement about any significant Activity carried out by a subsidiary, indeed we value openness and absence of ambiguity highly, when we do not credit a company with an Announcement, it should be assumed as a default that we are limiting ourselves to Activities of the parent itself and statements and reports made about the parent itself, rather than any subsidiary. We do attempt to extend the Activities we review to subsidiaries owned or controlled to the extent we are able to cover them, and to the extent public information exists.

When we refer to a company having made a Partial Announcement, we are comparing the limited information we able to obtain and monitor on that company’s Activities with those covered by any Announcement that we have monitored. Companies do not report in a uniform fashion on the relative significance of their Activities or on the Activities of their subsidiaries. This element of our work invariably involves us making our best judgment with the material that is available. For example, unless a company were to say, for example, ‘we have stopped activity X in Russia, historically it has generated Y% of our profits’, we have to make our own best judgment of how significant any given Activity is to the company before deciding how to assess and rate it.

Subject to the default assumptions to be made as set out above, our analysis and statements may therefore refer either to a) the parent or b) the parent and/or any of its subsidiaries or controlled subsidiaries; since it depends on the information that we have available to analyze. It should be recognized, due to the likely incompleteness of one or both of the information on Activities and the statements, that the comparison will not always be an ‘apples to apples’ one.

We do not and cannot identify all Activities that a company with multiple subsidiaries or controlled entities – sometimes these will be in the hundreds, might have in Russia. Our work does not involve investigations on the ground of what companies are doing, but on Announcements made by companies. Nor can we be aware of all statements the group may have made covering all of these Activities, in part because the company is not obliged to disclose its withdrawals from doing business with or in Russia and may not voluntarily do so, or also because significant Announcements may be made by subsidiaries alone which are difficult to find or to trace back to parents.

We are therefore not able to ascertain, and do not purport to report on, whether or not any Activity has been stopped ‘on the ground’ or somewhere in the parent company or the wider group. Even for companies with few involvements, there can be difficulties in finding information as to what is happening on the ground or in the group, so we have not sought it out. Therefore, any of our statements about stopping involvement with Russia are based on available information about Announcements and we specifically remind readers of our definition of Announcements, which is the base of everything we monitor and state. Thus, we are not making claims as to what a company has or hasn’t done beyond an Announcement. Because of the difficulties of knowing all information about companies, we refrain from stating that companies have definitively not stopped Activities, or rating them on that basis, and instead treat them according to whether they have made an Announcement based on its definition. Note that, when awarding a zero score for Degree, it very clearly does not mean that a company has not ceased doing business in or with Russia to some extent, and it should not be read as asserting that the company has made no change to its involvement with Russia, merely that it has not Announced the same.

For that reason, any company which has stopped Activities without announcing or publicizing that most likely will not be credited in our ratings and website. If a company wishes to be credited for itself or any relevant subsidiary in our system with a rating that reflects action it has taken to stop Activities with Russia, it must ensure that the same is published without ambiguity so that its position is reasonably ascertainable by those interested (such as our researchers). A company that, for whatever reason, fails to make its position clear, either on behalf of itself or a subsidiary, falls down in our rating for lack of proper disclosure or transparency, leaving aside its own actions relating to Activities.

Brands that are owned, controlled, invested in, affiliated with or that are otherwise reasonably associated with a company rated by us (the company is referred to as the ‘parent’ in all such cases for simplicity) are all given the parent’s rating, with the “associated” relationship indicated in the listing, regardless of whether the brand itself has any involvement with Russia or, if so, the status of its involvement. It is expressly stated that we attempt to inform consumers and media about the association of a brand with any company rated regardless of whether the associated company can control the decisions of the brand (or vice-versa), since it is nevertheless a way for the consumer to reward or punish rated companies with more leverage. Thus, the rating we associate with a brand is for consumers’ information and refers to the rating of the associated entity or parent.

The “Rating as of” date should be considered the date at which we have last tried to monitor information relating to a company and relating to other information we have published. Therefore, our information presented may be technically out-of-date if there have been developments since then. Reflecting this, any statements we make in the present tense refer to the “Rating as of” date. This ties in with our approach as to the importance of the first Announcement described under ‘Announcement’.

Our Verdicts, Moral Badges Moral Ratings, and the five-dimension scores underlying them (Degree, Speed, Attitude, Exposure and Power), represent our opinion based on facts we have collected or presented, which are themselves based on statements made by companies themselves or reports by reputable media, or based on the absence of Announcements, as we define them.

If we are unable to find information, we will do our best to make estimates to allow us to reach one or more of the scores and measures of the five dimensions. This is more commonly needed in Power and Exposure measurements, but it may sometimes be needed for other dimensions. A score of a dimension should not be construed to be a statement of fact but rather is an opinion and/or estimate of ours. We refer the reader back to ‘Incomplete Information’ above, which describes how we apply our judgment in certain instances and is indicative of our general approach.

We may revise the rating system if we identify improvements and will of course attempt to rerate affected companies accordingly to ensure standardized and comparable rating results.

Capitalized terms used on our site should be viewed in our Lexicon to get a more precise understanding of what we mean. See Lexicon.

At all times we have acted in good faith when dealing with these matters of great importance in the public domain. We have done our best to be as accurate as possible and believe our processes to be robust and fair. In particular, we have had a dedicated team of competent researchers looking hard for information published by and about companies relating to their involvement in Russia. Our view is that if a company’s information (or that of its subsidiary) about its approach to involvement with Russia after the invasion of 24 February 2022 is difficult to find, opaque, or ambiguous, then to a significant degree such a company has acted to bring criticism on themselves (or at the very least cannot expect to be credited with ratings or conduct that they consider would portray them in a good light but which they have rendered difficult to find).

That said, there may be circumstances, whether due to the vast amount of information available on complex and large companies and/or the lack of disclosure or clarity on the part of companies in relation to the range of Activities in or with Russia of theirs or their subsidiaries, and/or which Activities they are withdrawing from, or for whatever other reason, whereby we have missed a piece of information and/or, in good faith, presented something inaccurate or which a particular company may regard as unfair. We are very concerned to be a reliable and reputable resource. In such a case, we will make any necessary corrections on provision and consideration of reliable and clear information to the effect that there are any such errors, and we will also consider such new information in revising a rating and our information if we consider it will present a fairer picture of any company’s dealings (taking into account, of course, our view on the moral imperative for all companies to be open about their dealings with Russia).